On April 26, 2024, the draft Act implementing into the Polish legal system the provisions of the EU Directive on the principles of the global minimum tax (“Pillar 2”) was published. The purpose of the proposed Act is to implement in Poland, resulting from Council Directive (EU) 2022/2523, the principles of the global minimum tax. This means aiming for taxation with top-up tax on capital groups whose effective tax rate (“ETR”) is less than 15%.

According to the announcements of the Ministry of Finance, the Polish legal system will implement: the global top-up tax (in accordance with the IIR principle, i.e., the inclusion of income for taxation), the top-up tax on undertaxed profits (in accordance with the UTPR principle, i.e., the undertaxed profit rule), and the qualified domestic minimum top-up tax (QDMTT).

The draft regulations introducing the provisions of Pillar 2 are particularly important from the perspective of tax credits in force in Poland, which may lower the ETR below 15% for Polish taxpayers, thus triggering the obligation to pay a top-up tax (for entities headquartered in Poland, this may be the qualified domestic minimum top-up tax).

The draft Act will introduce new concepts regarding tax reliefs into Polish law, such as:

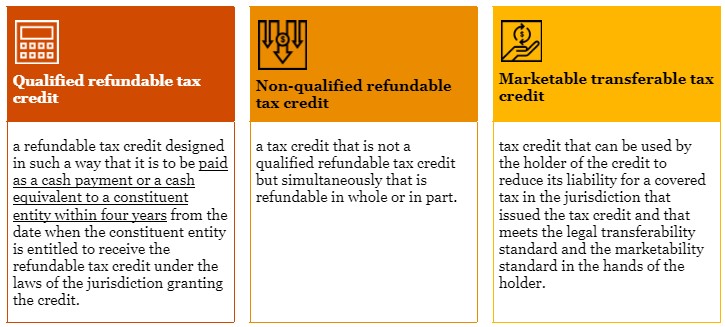

Qualified Refundable Tax Credit

According to GloBE rules, a qualified refundable tax credit must be refunded within 4 years of the entity meeting the conditions for the credit according to the regulations governing the use of that tax credit.

The legislator defines a refund as the payment of the unused amount of the tax credit in cash or cash equivalent. For the purpose of implementing Pillar 2 regulations, cash equivalents include, short-term government debt instruments, and anything else treated as a cash equivalent under the financial accounting standard used in the Consolidated Financial Statements as well as the ability to use the credit to discharge liabilities other than a covered tax liability.

For the purposes of calculating ETR, a qualified refundable tax credit is treated as qualified income, thereby potentially having a smaller negative impact on the ETR compared to a credit treated as a tax reduction. With less reduction of the ETR by qualified refundable tax credits, it is possible that using the tax credit will not trigger the obligation to pay a top-up tax or the tax will be lower than in the case of using non-qualified refundable tax credits.

Non-Qualified Refundable Tax Credit

Non-qualified refundable tax credits will primarily include tax credits refundable in whole or in part over a period longer than 4 tax years. Non-qualified refundable tax credits are also tax credits available only in the form of reducing the amount of qualified taxes.

For the purposes of calculating ETR, a non-qualified refundable tax credit is treated as a reduction of covered taxes, thus lowering the ETR level and potentially leading to the obligation to pay a top-up tax.

According to GloBE rules, it is first necessary to check whether a given tax credit meets the refund criterion; if it does not, it should be checked whether the tax credit can be considered a transferable tax credit (compliance with the transferability criterion is examined).

Marketable Transferable Tax Credit

As mentioned earlier, for a tax credit to be marketable transferable, it must meet the legal transferability and marketability standards. Both legal transferability and marketability standards should be considered depending on whether the holder acquired the primary or secondary right to the tax credit.

For an entity that acquired the primary right to the credit, the legal transferability standard is met when it is possible for an unrelated entity to acquire the right to the credit in the tax year in which the entity acquired this right or within fifteen months from the end of that tax year. In the case of entities that acquired the secondary right to the credit, the legal standard is met if it is possible, in the tax year of acquiring this right, for another unrelated entity to acquire it.

The marketability standard is met for an entity that acquired the primary right to the tax credit if the credit was acquired by an unrelated entity at a price equal to or higher than the minimum market price within fifteen months from the end of the tax year in which the entity acquired the right to the credit. For entities that acquired the secondary right to the credit, the market standard is met if the right was acquired from an unrelated person/entity at a price equal to or higher than the minimum market price. Regulations regarding qualified transferable tax credits also indicate that the minimum market price is 80% of the net present value (NPV) of the credit.

It should be noted that the refund or deduction due to a marketable transferable tax credit, or the expiration of the right to it, as well as the sale of this right, necessitates appropriate adjustments in the credit settlement.

For the purposes of the global minimum tax regulations, a marketable transferable tax credit is treated as income.

The mechanism of transferable tax credit has not been used in the Polish tax system so far, thus the potential introduction of credits meeting the definition of a marketable transferable tax credit will require the legislator to overhaul the current structure of tax credits. It should also be emphasized that there is currently no actual market for tax credits in Poland, which also prevents the treatment of Polish tax credits as marketable transferable tax credits.

Other Tax Credits

For tax credits that are not qualified refundable tax credits, non-qualified refundable tax credits, or marketable transferable tax credits, such credits are not included in the net accounting income (loss). Such reliefs for ETR purposes are treated as a reduction of covered taxes.

Implementation of Pillar 2 Regulations and Existing Tax Reliefs

The draft Act and existing regulations suggest that the current tax credits in Poland may be not generally considered qualified refundable tax credits. However, the interpretative practice in this area is yet to develop. If Polish tax credits were deemed non-qualified refundable tax credits, it would be a fundamentally unfavorable situation for taxpayers, as a non-qualified tax credit is treated as a tax reduction under Pillar 2 regulations. As a result, it has a greater potential to lower the ETR below 15%, leading to the obligation to pay a top-up tax.

In our opinion, the current structure of tax credits in Poland (e.g., the prototype credit or CSR credit) does not generally meet the refundability or transferability criteria. Nevertheless, it is worth noting that the mechanism of the innovative employees credit, which allows the remaining tax asset obtained under the R&D credit to be used for PIT advances of innovative employees, entitles taxpayers to use the R&D relief amount for PIT advances. Thus, the unused R&D credit is refunded as a cash equivalent in the form of reducing the PIT tax burden. When using the innovative employees credit, we see arguments for recognizing the mechanism as a refund of the R&D credit. Such an interpretation of the innovative employees credit mechanism provides grounds for potentially qualifying the R&D credit as a qualified refundable tax credit in the future. For this to happen, the legislator would have to adjust the refund period to the period under the Pillar 2 regulations (i.e., the asset generated in a given tax year should be used within the next 4 years).

Currently, the only act introducing changes to the structure of tax credits in the legislative work register is the draft of the so-called deregulation act, which proposes a favorable extension of the catalog of eligible costs in the R&D credit for taxpayers. Nevertheless, in light of the known practice of countries in implementing Pillar 2 regulations and public statements by representatives of the Ministry of Finance, we expect changes to the Polish tax credit system to adapt the credit mechanisms to the definition of qualified refundable tax credit or qualified transferable tax credit.

In our opinion, the R&D credit may be of particular importance in this context due to its significance for the development of the Polish economy (conducting R&D activities by entities enables industrial development, thereby providing consumers with better services and products, while process improvements allow cost optimization of production) and the significant savings that can result from its implementation in an enterprise (which may negatively impact the ETR level).

At the same time, we would like to point out that, for example, in Hungary, the R&D credit regulations have been adapted to meet the definition of a "qualified refundable tax credit." Thus, international practice and the announcements of the Ministry of Finance suggest that we can expect changes in the tax credit system that will minimize the negative impact of the global minimum tax on Polish taxpayers benefiting from tax credits.

We cannot rule out changes to the content of the draft Act implementing Pillar 2 after the consultations. The deadline for submitting comments on the draft has passed May 24, while according to the Ministry of Finance's announcements, the minimum global taxation regulations will come into effect on January 1, 2025.